I last wrote about pension superfunds two years ago. Amid the heightened sponsor risks associated with defined benefit (DB) pension schemes, on 18 June 2020, The Pensions Regulator (TPR) finally issued guidance on the financial, operations and governance standards it expects from DB superfunds. Whilst never replacing the strong employer looking to secure benefits in full in the foreseeable future, consolidators offer choice to sponsors or pension schemes newly in Pension Protection Fund (PPF) assessment who can only realistically hope to achieve funding above PPF levels (PPF+).

Bulk annuities have been popular

This new consolidation option is set against the background of a very active bulk annuity market. LCP figures show 2019 buy-ins and buy-outs hit a UK record at £43.8bn with a string of large blue-chip companies choosing this route. Their latest de-risking report suggests business will be £20-25bn in 2020 as schemes and sponsors look to secure pension member benefits in full. Thanks to the rise in gilt yields, bulk annuity prices are down 3-5% with no adjustment to mortality assumptions due to Covid-19.

Consolidation could suit an employer needing a clean break from their DB scheme in the short term due to corporate activity e.g. M&A, corporate restructure, renegotiating borrowing/raising debt or pension trustees who want an immediate improvement in security (typically but not always driven by concerns about the strength of the sponsor’s covenant). I thought this was summarised nicely in Rothesay Life’s 'The journey to buy-out' report.

Consolidation can be helpful

Covid-19 has had a huge impact on all areas of the economy, weakening many of the employer covenants behind DB schemes. The Pensions Minister, Guy Opperman, also recognises consolidation can help, saying the news was "…a big step towards a healthier and stronger pensions landscape. Well-run superfunds have the potential to deliver more secure retirement incomes for workers, while allowing employers to concentrate on what they do best - running their businesses."

A week later however, Sky News learnt Andrew Bailey (the new Bank of England Governor) had written to the Work and Pensions Secretary, Therese Coffey, to criticise elements of the interim framework. By not adhering to standards aligned with the EU's Solvency II framework for insurance companies, the Bank of England governor is understood to have said pension superfunds would be potential beneficiaries of ‘regulatory arbitrage’. As far as I know, no response has yet been seen.

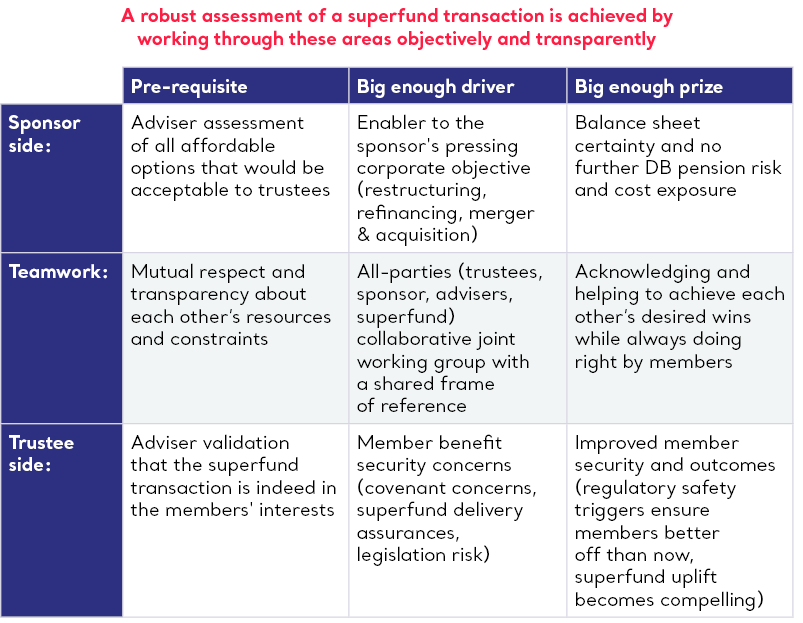

What The Pensions Regulator thinks

TPR hasn’t commented specifically but has stated, "We are fully alive to the risks presented by unregulated DB consolidator superfunds and other new models which are already being set up. Protections for savers are needed now which is why we have set a high bar for how they must show they are well-governed, run by fit and proper people and are backed by adequate capital." TPR added its modelling illustrates "there is a 99% likelihood the superfund would be able to pay the benefits they are promising to members in full."

Each transaction will require clearance by TPR and they will shortly publish a handy guide for pension trustees. The key considerations have been summarised by The Pension SuperFund in their graphic below:

A cost/protection trade off

In a recent session with Mercer I heard, depending on the DB scheme, superfunds believe the cost of transferring a scheme’s liabilities to them will typically be around 5-15% below the cost of an insurance company buy out. However, a key difference is the trade-off in the level of protection for members.

The first two consolidators, Clara and The Pension SuperFund, have quite different business models. Both will now seek regulatory approval to start taking on business this year, and more are expected to enter the market. Recent estimates have said DB schemes that can't reasonably hope to reach buyout within five years without a fresh capital injection but are funded to c85% of discontinuance valuations could be in range for consolidators.

Consolidators offer a capital buffer provided partly by the ceding sponsor to top up the solvency and from their respective backers at say 1/3:2/3 ratios as a rule of thumb. Economies of scale are also expected through the consolidation of investment and administration to reduce charges.

A quick take off?

A Willis Towers Watson client survey shows 9% are planning to proceed to consolidation with another 10% discussing it. The Pension SuperFund has already indicatively priced over £25bn of transactions, many of which are now progressing, and have seen new in-bound enquiries exceeding £1bn per week since the TPR guidance was published. A quick take off? I think so!

‘ PSGS & 20-20 Trustees merge to form Vidett ’

Punter Southall Governance Services (PSGS) & 20-20 Trustees (20-20) have today announced they...

‘ Don’t be surprised that your gilt funds are being treated like an emerging market ’

You may have seen or heard about the article in the Financial Times about how Insight...

Vidett is a trading name of Vidett Governance Services Limited, Vidett Trust Corporation Limited & Vidett HRT Limited

Registered in England and Wales numbers 3021321, 10842337 & 745598

Registered office: 3rd Floor Forbury Works, 37-43 Blagrave Street, Reading, RG1 1PZ